A “short sale” is when you sell your house at a price that is lower than

the balance you owe on your house. Because the proceeds from the sale

of your house falls short of the principle balance you owe the bank, it

is referred to as a “Short Sale”. This type of sale occurs when a

homeowner cannot afford the mortgage payments and the value of the

property drops so that the homeowner cannot refinance his home. The

Bank decides that selling the property at a loss is better than forcing

you into foreclosure.

The Banks have loss mitigation departments that will look at each

deal and decide if the bank will agree to a short sale. Each Bank will

have their own requirements for approving a short sale. Typically a

Bank will have the home appraised and based on that appraisal they will

decide if it is better to have you sell the home for less than you owe

or if they will make more money foreclosing on you and then selling the

house themselves.

If the Bank does agree to the short sale you are still not out of the

woods. You will still be responsible for the difference between the

short sale proceeds and the remaining balance of your mortgage unless

you have it clearly stated in the agreement that you are not responsible

for any remaining balances. Even after you get the Bank to forgive

the debt you sill have to deal with the Internal Revenue Service (IRS).

When you have any debt “forgiven” the IRS considers it to be income.

So while you are losing you house because you can’t afford to make the

payments the government expects you to pay taxes on the gains you

receive. You should always ask a tax professional what the impact of

the Short Sale will have on your personal income taxes since there are

some exclusions that have recently been put into effect.

Hopefully, the goal of making the definitions of a Short Sale Simple

has been achieved. You should seek the services of a licensed real

estate professional that specializes in Short Sales before you contact

the bank. These Professionals can negotiate with the Bank for you.

Also remember to consult with a tax specialist before signing any

agreement. by Mike Conrad

Brentwood TN short sale specialist

Sunday, April 28, 2013

Saturday, April 27, 2013

short sale homes

We represent a number of short sale properties. These can present a

great opportunity for the right buyer. Look to the right and you will

see a number of short sale homes. If you are an investor or looking for

a great deal, a short sale, pre-foreclosure or foreclosure may be right

for you. Give me a call on 615.429.6785 or email me at mike@mikeconrad.net

and let's begin your search today. We have Brentwood TN short sale

homes, Franklin TN short sale homes, Williamson County short sale homes

and Spring Hill TN short sale homes. We also have Nashville short sale

homes, Bellevue short sale homes and more short sale homes.

If you are already working with a REALTOR please be aware that all sales are subject to the seller's lender approval. Buyer's Agent will receive between 1 - 3 percent cooperating compensation depending on final approval of the short sale by the lender.

by Mike Conrad

what is a short sale home?

If you are already working with a REALTOR please be aware that all sales are subject to the seller's lender approval. Buyer's Agent will receive between 1 - 3 percent cooperating compensation depending on final approval of the short sale by the lender.

by Mike Conrad

what is a short sale home?

Thursday, April 25, 2013

Short Sales in Brentwood TN 37027

Someone help me out here, I am struggling to understand some of my fellow REALTORS and their buyers here in Brentwood TN 37027. I have a lovely home listed as a Brentwood TN short sale. It is a approved, cooperative short sale with a list price (lender approved and directed) of $485,000. Yes, the home needs some work, but why in the world would someone offer $345,000.00 when they knew I already had an offer of $460,000.00???

Why do REALTORS not do a better job of educating their buyers on the logic and structure behind the sale of a short sale home? I have worked hard to educate my short sale buyers that going after a short sale is not a way to get way more house than you could ever possibly afford without the short. That becomes a recipe for disaster as the day to day expenses of running a home otherwise way over your budget eventually catches up to you. Rather, when looking at a short sale, stay within the general confines of your budget, maybe a little over and go and get a really good price for that home.

example bad way only approved for a loan/purchase price of $400,000 don't go looking at $500,000 - $700,000 and try to get it for $400,000.

correct way same approval as above, look at homes priced at or below $425,000. assuming that the listing agent knows what they are doing, you might be able to get this short sale home for $375,000 - $400,000

Give me a call if you need to list or want to buy a short sale home in Brentwood TN 37027

by Mike Conrad

short sale homes in Brentwood TN

short sale homes in Brentwood TN

Why do REALTORS not do a better job of educating their buyers on the logic and structure behind the sale of a short sale home? I have worked hard to educate my short sale buyers that going after a short sale is not a way to get way more house than you could ever possibly afford without the short. That becomes a recipe for disaster as the day to day expenses of running a home otherwise way over your budget eventually catches up to you. Rather, when looking at a short sale, stay within the general confines of your budget, maybe a little over and go and get a really good price for that home.

example bad way only approved for a loan/purchase price of $400,000 don't go looking at $500,000 - $700,000 and try to get it for $400,000.

correct way same approval as above, look at homes priced at or below $425,000. assuming that the listing agent knows what they are doing, you might be able to get this short sale home for $375,000 - $400,000

Give me a call if you need to list or want to buy a short sale home in Brentwood TN 37027

by Mike Conrad

Monday, April 22, 2013

Housing market starts

|

|

||

|

|

"I'm always making a comeback but nobody ever tells me where I've been." Billie Holiday.

And the evidence continues to show that the housing market is making a

comeback. Read on for details and what they mean for home loan rates.

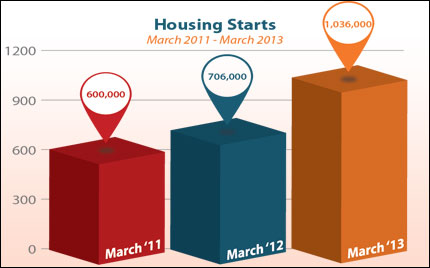

Housing

Starts spiked by 7 percent in March to 1.036 million units on an

annualized basis, well above the 930,000 expected. This was the largest

rate since June 2008. In addition, Housing Starts were up a whopping 47

percent since the same period last year. Housing

Starts spiked by 7 percent in March to 1.036 million units on an

annualized basis, well above the 930,000 expected. This was the largest

rate since June 2008. In addition, Housing Starts were up a whopping 47

percent since the same period last year.Building Permits, a sign of future construction, did decline by nearly 4 percent to 902,000. But overall, this was a strong report and further evidence of improvement in the housing sector. In other news, the Labor Department reported that the Consumer Price Index (CPI) declined by 0.2 percent in March, showing that inflation at the consumer level remains tame. Weekly Initial Jobless Claims rose by 4,000 to 352,000, with no clear signs of any significant move lower as the labor market continues to muddle along with no meaningful growth. And in the manufacturing sector, the Empire Manufacturing Index was much weaker than expected, falling to 3.1 in April from 9.2 last month. What does all of this mean for home loan rates? The Fed has noted that inflation remains in check and they expect this to continue for some time. The recent inflation and weak jobs data gives the Fed cover to continue its Bond purchase program known as Quantitative Easing, which should continue to benefit Bonds and home loan rates (since they are tied to Mortgage Bonds). The bottom line is that home loan rates remain near historic lows and now is a great time to consider a home purchase or refinance. Let me know if I can answer any questions at all for you or your clients. |

|

|

|

|

|

|

|

Forecast for the Week

|

|

|

|

|

|

|

|

|

This week contains a full slate of important news from start to finish.

In

addition, earnings season continues and the markets will be watching

these reports closely for signs regarding whether our economy is

improving.

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. The chart below shows Mortgage Backed Securities (MBS), which are the type of Bond that home loan rates are based on. When you see these Bond prices moving higher, it means home loan rates are improving -- and when they are moving lower, home loan rates are getting worse. To go one step further -- a red "candle" means that MBS worsened during the day, while a green "candle" means MBS improved during the day. Depending on how dramatic the changes were on any given day, this can cause rate changes throughout the day, as well as on the rate sheets we start with each morning. As you can see in the chart below, Bonds and home loan rates remain near record best levels. I'll continue to monitor this closely.

Chart: Fannie Mae 3.0% Mortgage Bond (Friday Apr 19, 2013)

|

|

|

|

|

|

|

|

The Mortgage Market Guide View...

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

Five Ways to Get More Business From Your Website

Many small to midsize local businesses have ineffective websites and often still rely on traditional media to get leads and drum up new clients. But online search analysis company Chitika reports over 43 percent of all internet search queries are now local. Combine this with declining readership in print publications and Yellow Page use, and local businesses may be looking at a serious problem. Here are five ways to make sure your website keeps up with the rapidly changing face of technology: Go mobile. According to Google and Bing, over 50 percent of web searches made from a mobile device are local and yet 93.3 percent of local business websites are neither mobile compatible nor render correctly from most smartphones. Mobile compatibility is critical as customers will usually move on to the next site within a few seconds if they are required to "pinch and zoom" for information. Be social. According to Marketecture, Inc., a company providing websites for small businesses, 80.5 percent of small businesses don't provide social media links on their website, even if they have a social media presence. Social media is potentially one of the largest sources of free traffic, so make sure your website communicates your presence there. Answer quickly. Email is convenient, fast, and ubiquitous. Getting in touch with you should be the same. Make sure your website has contact information, including email, where it can be easily seen on every page of your website. The same is true for your phone number: make sure it's everywhere on your site and not just the Contact page. Be a resource. If you don't have an "information request" form on your website, connected to both your email and CRM, you're missing out on a great avenue for leads. Make it easy for people to ask questions and receive quick answers, and you will always be rewarded with new business and stronger referrals. SEO is essential. Woody Allen once quipped that 80 percent of success is just showing up. But if your website doesn't show up in search results, you're 100 percent out of the race. A significant source of customers can result from the traffic directed to you by search engine results. Search engine optimization (SEO) using proper keywords, site optimization, and link building are necessary to get search engine ranking. If you don't know how to do it yourself, it's worth hiring specialists. Address these areas on your website and you'll capture a bigger share of local website traffic, improve your customer engagement and, of course, get more leads and new business coming in the door than ever before. Please pass this along to any clients and colleagues who might benefit from these tips.

Economic Calendar for the Week of April 22 - April 26

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

The

material contained in this newsletter is provided by a third party to

real estate, financial services and other professionals only for their

use and the use

of their clients. The material provided is for informational and

educational purposes only and should not be construed as investment

and/or mortgage advice. Although the material is deemed to be accurate

and reliable, we do not make any representations as

to its accuracy or completeness and as a result, there is no guarantee

it is without errors.

As your mortgage professional, I am sending you the

MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you.

In the unlikely event that you no longer wish to receive these valuable market updates, please

USE THIS LINK or email:

Craig.E.Newby@Wellsfargo.com

If you prefer to send your removal request by mail the address is:

License# 450444

Wells Fargo Home Mortgage

Friday, April 19, 2013

Referrals For Nashville TN short sales

Got a call yesterday from a REALTOR in Colorado asking me if I would take on a referral short sale in Nashville TN. of course i said i would, i love having someone find me on the internet and refer business. We talked a bit about short sales and my methodology toward selling homes under a short sale environment.

part of my process in selling a short is getting the homeowner in the right mindset to let the process work as efficiently as possible. we all know by its very nature a short sale is a tedious and trying undertaking, but can be done if everyone (buyer and seller and their respective agents) enter into it with the right mindset and same goal. that being, get the home sold for a fair price with the lender's blessing and minimize the strain and stress on everyone.

more to come on this one

by mike conrad

short sale homes in nashville tn

part of my process in selling a short is getting the homeowner in the right mindset to let the process work as efficiently as possible. we all know by its very nature a short sale is a tedious and trying undertaking, but can be done if everyone (buyer and seller and their respective agents) enter into it with the right mindset and same goal. that being, get the home sold for a fair price with the lender's blessing and minimize the strain and stress on everyone.

more to come on this one

by mike conrad

short sale homes in nashville tn

Thursday, April 18, 2013

HARP extended

Good news for the Brentwood TN, Franklin TN and Williamson County TN home market.

The Federal Housing Finance Agency (FHFA) has announced the extension of the Home Affordable Refinance Program (HARP) by two years to December 31, 2015

Finding a Top Agent to list and sell your home

The Federal Housing Finance Agency (FHFA) has announced the extension of the Home Affordable Refinance Program (HARP) by two years to December 31, 2015

Finding a Top Agent to list and sell your home

Wednesday, April 10, 2013

What is a Short Sale??

What is a Short Sale? A

short sale is when the bank agrees to take less than what is owed on

the mortgage to close on the sale of a home.(there are not fees to the

seller) A short sale is a common solution for people that owe more than

their home is worth, can't afford the monthly payments or don't have

the money to bring to closing to complete the sale of their home. PLUS

a lot of banks are now paying home owners as much as $5,000 to $30,000

for relocation costs if they maintain the home during the sale! They

pay this because it’s cheaper than the foreclosure process!

(We are not licensed attorney's or CPA's so cannot advise on tax consequences but there is relief if you sell short, see Mortgage Forgiveness Debt Relief Act of 2007. The IRS could consider the loss as income but the tax act may forgive it!)

There is no cost to you and we will never ask you for any money at anytime!

The

bank will pay our compensation for getting the property sold. At the

same time we will look out for your interests and take the pain and

confusion out of doing a short sale. We provide, at no cost to you, an

ethical and professional solution. While it is possible to negotiate on

your own most often the bank will want your property listed with a real

estate professional.

I have done many short sales so we can guide you through the process. Many times it takes 60 - 90 days and hours of time spent on the phone tracking down the right people and processing the deal. You do not want to risk losing a buyer due to long processing times. (No money comes out of your pocket since the bank takes less than what is owed.)

THE KEY TO A FAST, SUCCESSFUL SHORT SALE IS TO TAKE THE TIME UP FRONT AND GATHER ALL OF THE PAPERWORK WE'LL NEED TO PROCESS THE TRANSACTION.

Tuesday, April 9, 2013

Nashville TN Short Sales

Short Sale and Foreclosures in Brentwood TN

Short Sale vs. Foreclosure? What are the Consequences

You make the call!

I get the question from people all the time: short sale or foreclosure, which is the better option? My knee-jerk reaction is always “Are you kidding? Short sale, of course!” This has been mostly because I was always under the impression that a short sale, although still a ding on your credit, was gentler on the score than a foreclosure.But according to a recent blog post by FICO Banking Analytics, there is no real difference in the affect a short sale or a foreclosure has on your credit score. Both the impact in points and the time to fully recover is about the same for both events.

This put me in a precarious situation. All this time I had lauded the short sale as vastly superior to foreclosure, largely because of its less adverse affects on credit. So I was forced to do further research into which was the better option. In doing so I learned about benefits of a short sale I wasn’t even aware of, and found that the FICO blog was way off.

Each borrower’s credit situation is different, and the way that a creditor reports a short sale to bureaus is different. The reality is that hundreds of thousands of distressed Nashville homeowners who have chosen a short sale have experienced a lesser impact on their credit than those who have chosen foreclosure.

Here is the big difference: In a short sale, some or all of the debt could be completely forgiven, wiped out, and gone forever! In a foreclosure, the debt could be hanging over a homeowners head for years. A short sale allows the homeowner to control how the remaining debt, i.e. the deficiency balance, will be handled. This is huge as it could impact a homeowners financial future for years to come.

In a short sale, a distressed homeowner may be able to obtain another mortgage sooner than someone who has a foreclosure on his or her record. Also, more and more employers pull credit before hiring a potential employee, and a foreclosure can keep you from getting a job. Some employers pull credit reports on existing employees, and a foreclosure may not bode well in certain industries.

These benefits stacked against the negatives of foreclosure, including the embarrassment of public announcement and literally being kicked out of your home, make, in my opinion, short sale the reigning champion.

Monday, April 8, 2013

DON'T JUST SIT THERE, GET OUT THERE AND SELL SOMETHING!!

COMPLIMENTS OF JOHN WATKINS WITH NASHVILLE HOME INSPECTIONS

Read

On And Rock On!

Seven Decisions that Determine

Personal Success

Van DeebYou have the ability to incorporate into your life these seven decisions that will determine your personal success. Here are very brief excerpts of each decision; I hope you enjoy them as much as I do.

I have never met Andy Andrews, the author of one of my new favorite books, The Traveler’s Gift. However, I feel a very deep connection with his story of the seven decisions that determine success. His book is, by far, one of the best self-development, motivating, and inspirational books I have ever read (besides Common Sense Selling).

Reading about these decisions motivated and inspired me so much that I decided to share some of the main points with you.

You have the ability to incorporate into your life these seven decisions that will determine your personal success. Below are very brief excerpts of each decision; I hope you enjoy them as much as I do.

1. THE BUCK STOPS HERE: I will not let my history control my destiny. I accept responsibility for my past. I am responsible for my success. My decisions have always been governed by my thinking. I control my thoughts. I control my emotions. My thoughts will be constructive, never destructive.

2. I WILL SEEK WISDOM: I will train my eyes and ears to read and listen to books and recordings that bring about positive changes. I will read and listen only to what increases my belief in myself and my future. I will choose to associate with people whose lives and lifestyles I admire. I will listen to the counsel of those who are wise. By learning from other people’s wisdom, I add their knowledge and experience to my own and dramatically increase my success. I will not look for someone to open my door; instead, I will seek to open the door for someone else.

3. I AM A PERSON OF ACTION: I will create a new future by creating a new me. I inspire others with my activity. I am a leader. Knowing that laziness is a sin, I will create a habit of lively behavior. I will walk with a spring in my step and a smile on my face. My activity will create a wave of success for the people who follow me. As a leader, I have the ability to encourage and inspire others to greatness. I do not fear failure, because failure exists only for the person who quits. I do not quit. I am courageous. I am a leader. I seize the moment. I choose now.

4. I HAVE A DECIDED HEART: I am passionate about my vision for the future. The power to control my direction belongs to me. Today I will begin to exercise that power. I will awaken every morning with an excitement about the new day and its opportunities for growth and change. Yes, I have a dream. It is a great dream. My hopes, my passions, my vision for the future are my very existence. A person without a dream never had a dream come true. My course has been charted, and my destiny is assured.

5. TODAY I WILL CHOOSE TO BE HAPPY: Happiness is a choice. I am enthusiastic about each day. I am alert to its possibilities. I will become the master of my emotions. I will greet each day with laughter. I know that enthusiasm is the fuel that moves the world. The world belongs to the enthusiastic, for people will follow them anywhere! My smile has become my calling card. It is, after all, the most important weapon I possess. I am the possessor of a grateful spirit.

6. I WILL GREET THIS DAY WITH A FORGIVING SPIRIT: By the act of forgiving, I am no longer consumed by unproductive thoughts. I will forgive those who have criticized me unjustly. I now understand that forgiveness has value only when it is given away. I forgive their lack of vision, and I forge ahead. I now know that criticism is part of the price paid for leaping past mediocrity. I will forgive those who do not ask for forgiveness. From this day forward, my history will cease to control my destiny. I have forgiven myself. My life has just begun.

7. I WILL PERSIST WITHOUT EXCEPTION: I possess the greatest power ever bestowed upon mankind. I hold fast to my dreams. I stay the course. I do not quit. I acknowledge that most people quit when exhaustion sets in, but I am not “most people.” I am stronger than most people. Average people compare themselves with other people, and that is why they remain average. I compare myself to my potential. I am not average. I see exhaustion as a precursor to victory. By persisting without exception, my outcome—my success—is assured.BUYING AND SELLING HOMES IN BRENTWOOD TN, FRANKLIN TN AND WILLIAMSON COUNTY TN

Saturday, April 6, 2013

Selling Luxury Homes

If you’re looking to sell your

luxury home this summer, it might be a challenge with the current

economy to close the deal quickly. There is good news however, many

people are currently buying homes, and if you need to sell, there is a

fairly good chance of finding a buyer for your home. To help you sell

your home quicker, there are some simple things you can do to not only

maximize your home’s value, but also close the deal faster.

First

impression is everything. A buyer can sometimes decide whether he is

even going to consider placing an offer on your home in the first thirty

seconds. Since the outside is the first part of your home a buyer

views, increase your curb appeal. Take extra care to manicure your lawn,

plant fresh flowers, and clean your yard of any junk. A thorough

cleaning of the inside of your home is important before showings; nobody

likes a dirty or smelly home.

First

impression is everything. A buyer can sometimes decide whether he is

even going to consider placing an offer on your home in the first thirty

seconds. Since the outside is the first part of your home a buyer

views, increase your curb appeal. Take extra care to manicure your lawn,

plant fresh flowers, and clean your yard of any junk. A thorough

cleaning of the inside of your home is important before showings; nobody

likes a dirty or smelly home.- Stage your home! On average staged homes sell for 6-10% more than their counterparts and almost twice as fast. Consider hiring a professional in order to prep your house for showings. Even small items as fresh flowers or removing personal items make a huge difference in the buyers mind.

- Don’t waste your time with unqualified buyers. When selling luxury homes in Middle Tennessee unfortunately there are heaps of potential buyers looking for luxury living accommodations that they simply can’t afford. Have your realtor make sure buyer who are submitting offers are first qualified before considering them. This will not only save your time, but also keep you from experiencing an emotional rollercoaster.

- Make sure you highlight the focal points and amenities of your home. Luxury homes are about one thing, luxury. If you have a pool, hot tub, tennis courts or other luxury features, make sure they are marketed to prospective buyers. These features make the difference in the sales of luxury homes.

- Hire a realtor that is familiar with not only the area but luxury real estate as well. The sale of luxury homes can be more complex and require specific attention to certain details than your average home. Your realtor should be knowledgeable in luxury home construction, negotiation, as well as financing in order for you to fetch top dollar for your property.

all about Williamson County TN, Brentwood TN, Franklin TN, Davidson County TN and Greater Middle TN homes and living

here's a great link to all kinds of info for the above

http://mikeconrad.featuredwebsite.com/schools.asp

http://mikeconrad.featuredwebsite.com/schools.asp

about MIke Conrad Brentwood TN and Franklin TN homes for sale

- Mike is a veteran sales executive with over 25 years of success and experience.

- Mike has held numerous senior

positions with companies in both the U.S. and Canada including Regional

Vice President at a major telecommunications company.

- Mike is a member of the National

Association of REALTOR (NAR), The Greater Nashville Association of

Realtors (GNAR) as well as the Franklin TN, Cool Springs and Brentwood TN

Chambers of Commerce.

- Mike is a licensed Broker in the State

of Tennessee. Mike is also accredited with

the National Association of Realtors as a Short Sale and Foreclosure

Resource (SFR). Mike is also a Corporate Relocation Specialist as well

as Luxury Home Specialist. Mike is also accredited under the Resource

Collaborative Specialist program specializing in "Divorced" houses. (RCS-D)

- Graduate - Leadership GNAR

- Multi-Million Dollar Producer!

- Full time REALTOR since 2005

- Mike and his wife Sue live in Brentwood TN. Their son, Zac, is a 2010 graduate of the University of Alabama with a Bachelor of Business Administration and majors in Intl. Business and Spanish. They are members of Brentwood United Methodist Church and are actively involved in the local swimming community.

kudos for short sales and other real estate activity

Mike,

I want to say a major "thank you" for all your help and guidance in the sales process of my home in Franklin TN. You have always been informed, professional, quick to follow up on requests and questions, and very helpful in the development and presentation of marketing materials and listing information that led to multiple showings and offers. Your professional experience was a key factor in my selection of you as my agent, and I was very fortunate to work with you. Again, thank you for all your service and I would highly recommend you to future, potential clients.

Jonathon Esarey

Franklin TN

Short Sale Homes in Brentwood TN and Franklin TN

"We gave you FIVE STARS on Zillow!"

"We decided to list our home in Brentwood TN and chose Mike to be our REALTOR. Mike went above and beyond what was expected of him. He worked tirelessly during the listing, marketing and negotiating process and we were very pleased with the results. He gave us top notch personal service and handled the entire process very professionally.

We would definitely recommend him to anyone looking for a first class REALTOR."

Peter and Chivon Dechelle

Friday, April 5, 2013

What is a Short Sale?

What is a Short Sale?

What is a short sale? A "Short Sale" or "negotiated

settlement" or "short pay" occurs whena Lender agrees to accept less than the amount owed to payoff a loan as an alternative to

foreclosure. If the property is worth less than the amount owed on the loan, then even if the

Lender forecloses and takes back the property; they know they are going to take a loss. We

can often convince a Lender that they will "do better" if they take less than what is owed now

rather than taking the property back by foreclosure and trying to sell it later.

How long will it take? The Short Sale negotiation process is a lengthy one. It may take

several weeks or more likely several months to get an approval. Many Lenders have several

layers of bureaucracy, insurers, and investors that we will have to maneuver through in order

to get the Short Sale approved. So it is important to be patient during this long process.

But my house is going to foreclosure, will I have enough time? Maybe, maybe not. Just

starting a Short Sale does not automatically stop a foreclosure. However, many times we can

convince a Lender to stop the foreclosure to let us attempt to negotiate the Short Sale. So,

while there are no guarantees, it is in your best interest to try the Short Sale.

Can I stay in the house? The key word in "Short Sale" is sale. The purpose of a Short Sale

is to get the property sold. This is not a program that can stop foreclosure and allow you to

keep the house indefinitely. It will be easier to sell the house if it is vacant, so you should

make plans to move as soon as possible.

How do I know this will work? You don’t. We cannot, have not, and will not make any

promises to you that the Lender will accept a Short Sale. Once you missed a payment, the

Lender is in charge and can proceed to foreclosure if they want to. But we know they do not

want to and we are very good at presenting alternatives to the Lender that they often prefer to

accept rather than foreclose. We are very good at what we do, but NO PROMISES or

GUARANTEES are being made as to whether or not the Lender will accept a Short Sale –

they may or may not.

Will I get any money from the sale? NO. A universal requirement of Lenders granting a

Short Sale is that the borrower will not get any proceeds from the sale of the property. The

Lender is going to take a loss on your loan – they are not going to let you get any money.

What happens if this doesn’t work? Your house will likely go to foreclosure. A Short Sale

is something we try after you have exhausted your other options.

What is the difference between a "RELEASE" and a SATISFACTION? A Release is

where the Lender may offer to "release" its security interest against the property in exchange

for less than the amount of the note. However, the remaining debt on the property is still owed. A

Satisfaction is where the Lender agrees to accept less than you owe on the balance of your

mortgage as a complete and final "satisfaction" of the debt and the mortgage lien on your

property.

If the Short Sale is successful, it is a win-win situation for all of us. You win because you save your credit from a tremendous hit since a foreclosure will remain on your credit for ten years. This makes buying another house impossible for a long time. And yes, you will have late payments showing on your credit report, but as long as foreclosure does not occur, after twelve months of good rental history, you will be able to get a new mortgage and buy a house once again. We win because once the short sale is approved, and we buy the property or find a buyer for the property and make our profit that way. Bottom line is, if you don’t win, neither do we! The Lender wins because they can dispose of the property quickly instead of holding onto a non-performing asset which in the long run hurts them financially. Besides, the Lender is in the business of lending money not selling real estate. by Mike Conrad

What is a Short Sale

Tax Consequences of a Short Sale

Tax Consequences of a "Short Sale" of Real Estate

vs. Foreclosure

April

22, 2010

©

2010 by Michael C. Gray, CPA

Our nation is now seeing the effects

of tightening mortgage credit after a liberal period. With increases in

interest rates for adjustable rate mortgages and the conversion to amortization

of principal for interest-only (or negative amortization) loans, home values

for homes favored by subprime borrowers (and even other homes) are collapsing,

and the debtors are either trying to "walk away" from their homes and

allowing them to be foreclosed or are making "short sales."

A

"short sale" is selling the home for less than the mortgage balance

and trying to get the lender to forgive the unpaid balance. This is a new use

of the term, and is not the definition for this item in the Internal Revenue

Code. In the tax law, a "short sale" is a sale of a borrowed item to

be replaced at a future date, usually a security. The only case that I know

about using the term "short sale" for this type of transaction is a

2008 decision, Stevens v. Commissioner.1 With the explosion of real estate short sales, we will

undoubtedly soon see more cases with them.

A reason for debtors to consider a

"short sale" instead of a foreclosure is to try to protect their

credit history.

How

are foreclosures (and deeds in lieu of foreclosure) taxed?

An important consideration in the

results of a foreclosure (or a deed in lieu of foreclosure) is whether the debt

is "recourse" or "nonrecourse." If the debt is

"recourse," the debtor is personally liable for the debt. If the debt

is "nonrecourse," the debt is only secured by the property, and the

debtor is not personally liable for the balance.

You should consult with an attorney

to determine the status of your mortgage. In California, most mortgages that

are used to purchase a residence are nonrecourse, but mortgages from

refinancing a previous mortgage are usually recourse.

When

a nonrecourse mortgage is foreclosed, the property is treated as being sold for

the balance of the mortgage.2 This is important because the gain from a foreclosure of a

principal residence may be eligible for the $250,000 ($500,000 for

jointly-owned marital property) exclusion.

For example, for foreclosure of a

nonrecourse debt,

|

Nonrecourse debt

|

$500,000

|

|

Tax basis (cost to determine tax

gain or loss)

|

300,000

|

|

Gain

|

$200,000

|

If the holding period requirements

are met and the residence was a principal residence, the above gain would be

tax-free.

(Note: The above example is for

consistency and contrast with the results for recourse debt. Most non-recourse

debt for a residence is purchase-money debt, and would not exceed the tax basis

(purchase price) of the residence. When the residence was a replacement

residence for a principal residence sold before May 7, 1997, the tax basis can

be less than the cost of the residence. Most of the mortgages for residences

acquired in that scenario have probably been refinanced and are now recourse

debt.)

For

recourse debt, the debt is only satisfied up to the fair market value of the

property. There is a sale up to that amount. If the lender forgives the balance

of the mortgage, there is cancellation of debt income, which is taxed as

ordinary income.3 (Regulations § 1.61-12.) (But see tax relief enacted for

certain recourse debt secured by a principal residence, below.)

For example, for foreclosure of a

recourse debt,

|

Recourse debt

|

$500,000

|

|

Fair market value

|

450,000

|

|

Cancellation of debt (ordinary

income)

|

$

50,000

|

(If the cancellation of debt was for

"qualified principal residence indebtedness," it will be excluded

from taxable income. If the taxpayer still owns the home after the cancellation

of debt, the excluded amount will be subtracted from the tax basis of the

residence. See the section on "tax relief," below.)

|

Fair market value

|

$450,000

|

|

Tax basis

|

300,000

|

|

Gain

|

$150,000

|

Again, if the holding period

requirements are met and the residence was a principal residence the above gain

would be tax-free, but the cancellation of debt would generally be taxable as

ordinary income, except for certain "qualified principal residence

indebtedness." See the section on "tax relief," below.

Tax

relief enacted for recourse mortgage on principal residence debt forgiveness.

Congress has passed and President

Bush has approved H.R. 3648, the "Mortgage Forgiveness Debt Relief Act of

2007." The legislation is effective for discharges of indebtedness on or

after January 1, 2007 and before January 1, 2010. The Federal Bailout

Legislation H.R. 1424, passed on October 3, 2008, extended this relief through

December 31, 2012.

Under the new law, a discharge of

"qualified principal residence indebtedness" is excluded from taxable

income. "Qualified principal residence indebtedness" is acquisition

indebtedness secured by the principal residence of a taxpayer as

defined for the deduction of residential mortgage interest, but the limit is

$2,000,000 for the exclusion ($1,000,000 for the mortgage interest deduction)

and $1,000,000 for married persons filing a separate return ($500,000 for the

mortgage interest deduction). Also, the exclusion only applies to a mortgage

secured by the principal residence of the taxpayer.

The

election to exclude the income from discharge of principal residence

indebtedness is made on Form 982 (Re. February 2008), Part I, lines 1.e and 2.

According to IRS Publication 4681, a basis reduction amount is entered at Part

II, like 10.b. only if the taxpayer still owns the residence after the debt

cancellation.4 IRS Publications aren't considered legal authority and I

haven't found any other authority for not making a basis adjustment when the

debt cancellation happens at the same time as a foreclosure or short sale.

The exclusion does not apply if the

discharge relates to providing services to the lender or any other factor not

related to a decline in the value of the residence or the financial condition

of the taxpayer/borrower.

According to IRS Publication 4681,

if the taxpayer continues to own the home after the debt cancellation, the tax

basis of the residence (cost used to determine taxable gain or loss on sale) is

reduced by any amount of discharge of indebtedness excluded from taxable

income, but not below zero. There is no basis adjustment if the debt

cancellation happens with a foreclosure or short sale. There will be two

calculations. (1) Cancellation of debt income eligible for exclusion. (2) Sale

of residence to apply applicable exclusion.

The new exclusion of income for

discharge of acquisition indebtedness for a principal residence takes

precedence over the exclusion relating to insolvency (discussed below), unless

the taxpayer elects otherwise.

For example, if the previous example

for a recourse debt was eligible for the exclusion, here are the tax results:

|

Recourse debt

|

$500,000

|

|

Fair market value

|

450,000

|

|

Cancellation of debt excluded from

taxable income

|

50,000

|

|

Fair market value

|

$450,000

|

|

Tax basis

|

300,000

|

|

Gain

|

$150,000

|

If the holding period requirements

are met, the above gain would qualify for the exclusion ($500,000 married,

joint or $250,000 single) for sale of a principal residence.

(Remember the foreclosure of a

non-recourse mortgage is not a discharge of indebtedness, but a

"sale" of the residence in satisfaction of the mortgage. Therefore,

such a foreclosure won’t qualify for the new exclusion, but may qualify for the

exclusion of gain for sale of a principal residence. Also, since the balance of

acquisition indebtedness is almost always less than the tax basis (cost) of the

residence, it would be highly unusual for there to be a gain from a

foreclosure.)

An "ordering rule" in the

tax law says that the exclusion only applies to as much of the amount discharged

as exceeds the amount of the loan which is not qualified principal residence

indebtedness.5 The IRS explains how to apply the rule at Page 8 of

Publication 4681.

For example, Julie Smith’s residence

was foreclosed in 2008. The fair market value of her home was $200,000. The

balance of her mortgage was $275,000. Julie had used $50,000 from refinancing

her home to pay down her credit card debt, not for home improvements. $50,000

of the debt discharge that is not qualified residence debt would be taxable,

and the remaining $25,000 that is qualified residence debt would be excluded

from taxable income.

Another example, the residence of

John and Mary Taxpayers was foreclosed in 2008. The fair market value of their

home was $1,500,000. The balance of their mortgage, which was all acquisition

indebtedness, was $2,250,000. Since the maximum qualified principal residence

indebtedness is $2,000, 000, $250,000 of the debt was not qualified principal

residence indebtedness. The $250,000 non-qualified debt cancellation would be

taxable income, and the remaining $500,000 that is qualified indebtedness would

be excluded from taxable income.

Amounts that are otherwise taxable

in the above examples could qualify for exclusions under other exceptions, such

as for insolvency or bankruptcy.

California

extends debt cancellation tax relief for homeowners.

California has enacted relief

legislation for cancellation of mortgage debt relating to the acquisition of a

pricnipal residence.

Governor Schwartzenegger signed SB

401 (Wolk), the Conformity Act of 2010, on April 12, 2010, while we tax return

preparers were busy finishing income tax returns and extension forms.

Effective for taxable years 2009 through

2012, the maximum qualified principal residence indebtedness eligible for

relief is $400,000 for taxpayers who file as married or registered domestic

partners filing a separate return and $800,000 for taxpayers who file joint

returns, single persons, head of household and qualifying widow or widower

(other individual taxpayers). The federal limits are $1 million for married

persons filing a separate income tax return or $2 million for other individual

taxpayers.

The debt relief that can be excluded

from taxable income is limited to $250,000 for married or registered domestic

partners filing a separate return and $500,000 for other individual taxpayers.

The federal exclusion is limited to the amount of qualified principal residence

indebtedness.

Note that the amount that can be

excluded from taxable income for California was increased compared to the

amounts that could be excluded for 2007 or 2008, which was $125,000 for married

or registered domestic partners filing a separate return and $250,000 for other

individual taxpayers.

Those taxpayers who now qualify for

relief for 2009 and who filed their 2009 California individual income tax

erturns should file amended returns, Form 540X, including an amended Schedule

CA (540/540NR). When filing Form 540X, write "Mortgage Debt Relief"

in red across the top of page one of Form 540X.

There is no California equivalent

for Form 982, Reduction of Tax Attributes Due to Discharge of Indebtedness. use

the Federal form marked "California" at the top.

Remember the tax basis of the

residence is reduced for the excluded gain.

What

happens with a "short sale"?

Short sales are taxed under the same

rules as foreclosures.

Recourse debt cancellation is not

satisfied with the surrender of the property, so any debt not satisfied with

the sale proceeds would be taxable as cancellation of debt income, except for

certain "qualified principal residence indebtedness." See section on

"tax relief" above. (Rev. Rul. 92-99, 1992-2 CB 518. Also see

Treasury Regulations Section 1.1001-2(a)(2).)

Therefore, the tax consequences

would be similar to the "recourse debt" example, above. The buyer and

seller might also have legal concerns about whether the lender would consent to

the transaction and whether (for recourse debt) the lender would in fact

forgive the debt.

For example, for a recourse debt

short sale,

|

Net sale proceeds

|

$450,000

|

|

Tax basis

|

300,000

|

|

Gain

|

$150,000

|

|

Debt

|

$500,000

|

|

Pay off using net sale proceeds

|

450,000

|

|

Cancellation of debt (ordinary

income)

|

$

50,000

|

(If the cancellation of debt was for

"qualified principal residence indebtedness," it will be excluded

from taxable income and be subtracted from the tax basis of the residence. See

the section on "tax relief," above.)

For

non-recourse debt short sales when the seller and buyer require the

cancellation of the debt by the lender as a condition of the sale, the debt

cancellation is included in the sale proceeds, like for a foreclosure.6

Therefore, a "short sale"

can be a viable alternative to a foreclosure for debtors with nonrecourse debt

and who qualify for the exclusion from income of the gain from the sale of a

principal residence.

What

about selling expenses for a recourse mortgage?

For simplicity, I have disregarded

selling expenses in the above discussion. For a short sale, selling expenses

reduce the sales proceeds available to reduce the loan. For a foreclosure or

deed in lieu of foreclosure, selling expenses are added to the debt. (See Jerry

Myers Johnson v. Commissioner, TC Memo 1999-162, affirmed CA-4, 2001-1 USTC

¶ 50,391.) The net result should be similar, assuming the fair market value of

the property equals the selling price for a short sale.

For example, for foreclosure of a

recourse debt,

|

Recourse mortgage balance

|

$500,000

|

|

Selling expenses

|

50,000

|

|

Total debt

|

$550,000

|

|

Fair market value

|

450,000

|

|

Cancellation of debt (ordinary

income)

|

$100,000

|

(If the cancellation of debt was for

"qualified principal residence indebtedness," it will be excluded

from taxable income. According to IRS Publication 4681, if the cancellation of

indebtedness happened relating to a short sale, no basis adjustment would be

required. If the taxpayer still owned the hoome after teh debt cancellation,

the exclusion amount would be subtracted from the tax basis of the residence.

See the section on "tax relief," above.)

|

Fair market value

|

$450,000

|

|

Tax basis

|

-300,000

|

|

Selling expenses

|

-50,000

|

|

Gain

|

$100,000

|

For example, for a recourse debt

short sale,

|

Sales price

|

$450,000

|

|

Selling expenses

|

-50,000

|

|

Tax basis

|

-300,000

|

|

Gain

|

$100,000

|

|

Recourse mortgage balance

|

$500,000

|

|

Pay off using net sale proceeds

($450,000 sales price - $50,000 selling expenses) |

400,000

|

|

Cancellation of debt (ordinary

income)

|

$100,000

|

(Same caveat for "qualified

principal residence indebtedness" as above.)

Cancellation of debt income may not

be taxable if the debtor is insolvent or has the debt discharged in bankruptcy.7 With recent changes in the federal bankruptcy laws, it is

much harder for individuals to file bankruptcy than before the changes.

What

if the fair market value of the home has dropped after purchase?

Example - Non-recourse

foreclosure/short sale

|

Mortgage balance

|

$500,000

|

|

Tax basis

|

700,000

|

|

Loss

|

-$200,000

|

(The fair market value of the

property is disregarded for a non-recourse mortgage.)

If this is a principal residence,

the loss is a non-deductible personal loss.

Example – Recourse foreclosure/short

sale

|

Mortgage balance

|

$500,000

|

|

Fair market value

|

450,000

|

|

Cancellation of debt income

|

$

50,000

|

(But see the rules for exclusion for

cancellation of "qualified principal residence indebtedness" in the

section on "tax relief," above.)

|

Fair market value

|

$450,000

|

|

Tax basis

|

$700,000

|

|

Loss (for personal residence,

non-deductible)

|

-250,000

|

Senator

Grassley asks IRS to help homeowners with loan forgiveness tax bills.

Senator Chuck Grassley, R-Iowa, who

is the ranking minority member on the Senate Finance Committee, has sent a

letter to the Treasury Department and the Internal Revenue Service asking for

help for homeowners who face big tax bills because of home loan debt

forgiveness on a principal residence. Grassley asked that the IRS accept offers

in compromise to eliminate or reduce the taxes for these transactions.

Grassley reminded the IRS that they

may compromise to promote effective tax administration where compelling public

policy or equity considerations identified by the taxpayer provide a sufficient

basis for compromising the liability.

(Similar requests were ignored when

taxpayers suffered tax disasters relating to stock option transactions during the

stock market crash of 2000 and 2001.)

Considerations

for rental real estate

Owners of rental properties often

have accumulated suspended passive activity losses that can be applied against

the income from a debt cancellation with respect to the rental.

Losses from the sale of

income-producing properties may be deductible as ordinary losses under Internal

Revenue Code Section 1231. (The loss is reported on Form 4797.) The loss may

offset cancellation of debt income. If the property isn’t income producing, the

loss may be a capital loss, limited to capital gains plus $3,000.

Taxpayers other than C corporations

may elect to exclude cancellation of “qualified real property business

indebtedness” from taxable income. (Internal Revenue Code Sections 108(a)(1)(D)

and 108(c).) This is mostly debt incurred to acquire, construct, reconstruct or

substantially improve real property used in a trade or business. (Rental real

estate is not considered to be used in a trade or business.) Refinanced

debt up to the qualifying amount of a previous debt also qualifies. The tax

basis of depreciable real property is reduced for the excluded gain. The amount

excluded is limited to the adjusted basis of depreciable real property before

the discharge.

Exclusions for discharges of debt in

bankruptcy in a title 11 case and up to the amount of insolvency are also

available for cancellations of debt relating to investment real estate.

The tax basis of assets must be

reduced for the excluded gain.

(Thanks to Richard Ogg, EA, who

brought the Briarpark decision to my attention!)

P.S. For more information, watch

Michael Gray's interviews of attorney William Mahan for the Financial Insider Weekly,

"How Mortgage Modifications, Short Sales and

Foreclosures Work" and "Short Sales and Foreclosures - Tax

Consequences." Attorney Michael Malter of Binder

& Malter, LLP also discusses short sales in Michael Gray's interview for Financial

Insider Weekly, “What you should know about bankruptcy for individuals”.

There are also explanations about

foreclosures and cancellation of debt in IRS Publications 523, Selling Your

Home; 552, Taxable and Nontaxable Income; and 544, Sales and Other Dispositions

of Assets at www.irs.gov.

Also see the instructions for Form 982. The IRS also recently issued IRS

Publication 4681, Canceled Debts, Foreclosures, Repossessions and Abandonments.

For

the latest U.S. income tax developments relating to real estate, subscribe to Michael Gray, CPA's Real Estate Tax Letter. There is no charge or obligation to subscribe to this

email newsletter.

IRS Circular 230 Disclosure: As required by U.S. Treasury Regulations, you are hereby

advised that any written tax advice contained on this website was not written

or intended to be used (and cannot be used) by any taxpayer for the purpose of

avoiding penalties that may be imposed under the U.S. Internal Revenue Code.

1 Stevens v. Commissioner, T.C. Summary Opinion

2008-61, June 3, 2008 return

2 G. Hammel, SCt, 41-1 USTC ¶ 9169 return

3 Regulations § 1.61-12 ; return

4 IRS Publication 4681, page 7. return

5 Internal Revenue Code § 108(h)(4) return

6 Briarpark v. Commissioner, 5th Circuit, 99-1 US Tax Cases 99-1 ¶ 50,209, 1/6/1999; T.C. Memo 1997-298, 6/30/1997. Also see Treasury Regulations Section 1.1001-2. ;return

7 Internal Revenue Code Sections 108(a)(1)(A) and 108(a)(1)(B) ;return

2 G. Hammel, SCt, 41-1 USTC ¶ 9169 return

3 Regulations § 1.61-12 ; return

4 IRS Publication 4681, page 7. return

5 Internal Revenue Code § 108(h)(4) return

6 Briarpark v. Commissioner, 5th Circuit, 99-1 US Tax Cases 99-1 ¶ 50,209, 1/6/1999; T.C. Memo 1997-298, 6/30/1997. Also see Treasury Regulations Section 1.1001-2. ;return

7 Internal Revenue Code Sections 108(a)(1)(A) and 108(a)(1)(B) ;return

Subscribe to:

Posts (Atom)